CASH DRIVEN | A TIMES INVESTIGATION

Big banks entrusted money to GardaWorld. It secretly lost track of millions.

Brian Newell had been a manager at one of GardaWorld’s armored truck branches for about a year when a high-ranking supervisor called in 2018 with a bizarre order: Load all the coins stored at his branch in Connecticut onto a truck bound for Massachusetts.

Auditors from Bank of America were coming to Garda’s Dedham, Mass., branch to count money that Garda was being paid to protect.

And some of it was missing.

Newell’s Stratford, Conn., branch was relatively small. It held about $20,000 in coins belonging to Bank of America and two other banks, Newell said in an interview. He sent it all.

A few days later, Newell said, he learned it hadn’t been enough.

The shortage was so large, other New England branches had been told to send money as well.

As Garda’s armored trucks became ubiquitous on American roads, the international security contractor also moved into the little-known but growing business of storing money for U.S. banks. It took just eight years for Garda to become the industry leader, holding money for some of the largest banks in the world.

Behind that spectacular growth is an untold story of deception.

A Tampa Bay Times investigation has found that Garda lost track of millions of dollars inside its vaults, then concealed the missing money from the banks that were its clients.

Court records and interviews depict some of the vaults as chaotic places where employees routinely ignored protocol and lost money. Some were rife with unsolved thefts and lacked basic safeguards like high-quality security cameras.

Garda sends banks a daily accounting of their balance in each vault. But as cash went missing, some branches kept reporting that the money was there, the Times found.

High-level Garda executives became aware of the discrepancies as early as 2014, a company document obtained by the Times shows. They set out to tally how much was missing and estimated roughly $9 million, according to the document.

It’s not clear how Garda responded. But six former Garda employees confirmed to the Times that Garda’s vaults were missing money in later years.

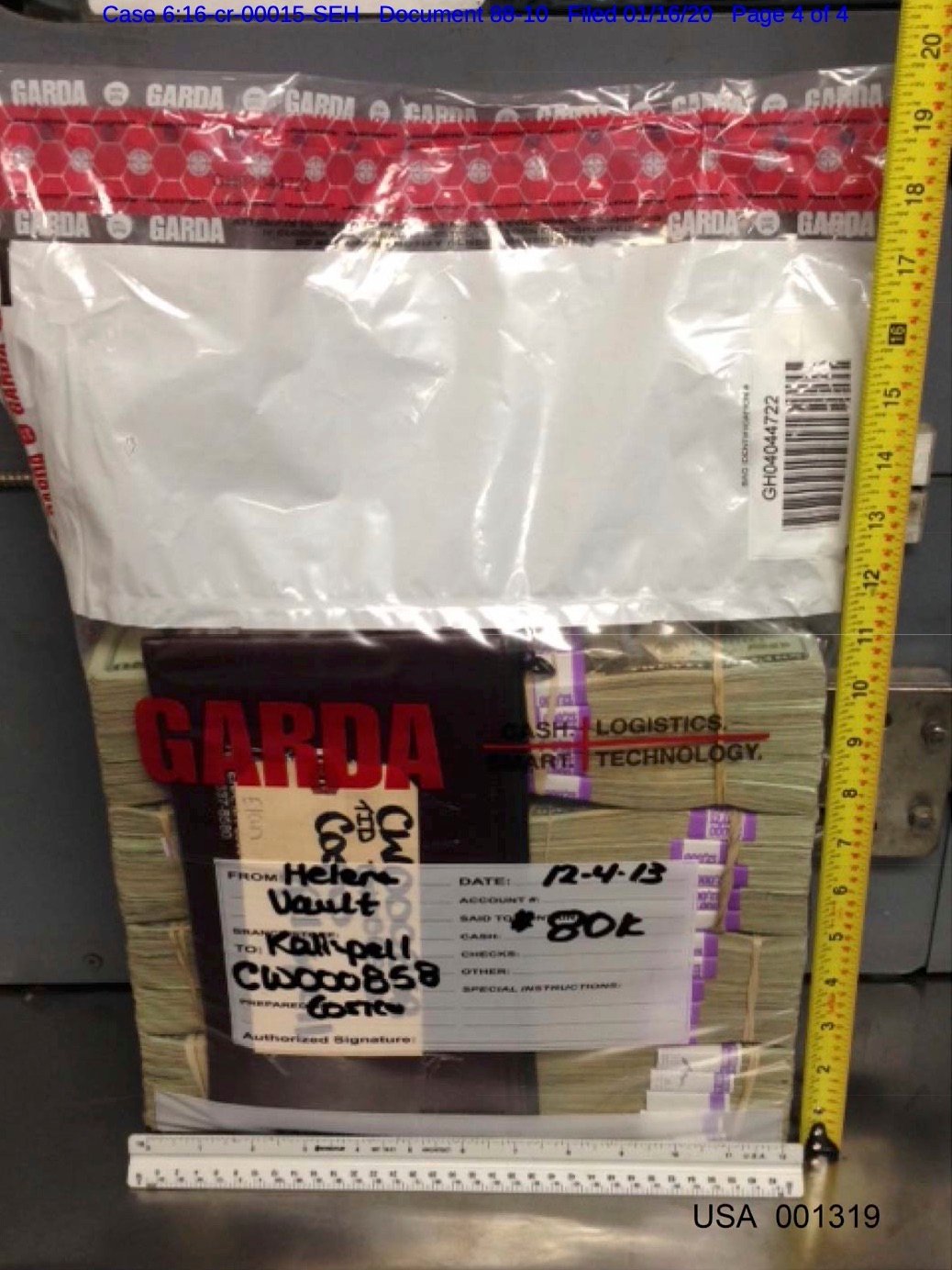

In 2015, emails show that Garda employees discussed how to keep TD Bank from learning that a single branch couldn’t find $924,000 of the bank’s coins.

In 2017 and 2018, employees in St. Louis repeatedly stalled bank auditors in a conference room while workers scrambled to move boxes of quarters and dimes — each containing hundreds of dollars — from one bank’s account to another, according to Jammie Bolton, the branch’s manager at the time.

Auditors were then shown the amount they expected. But they were unknowingly looking at another bank’s money, he said.

“They would pretty much bamboozle the auditors, when in fact they have no clue where the money is,” said Newell, who ran the Stratford branch. He said Garda terminated him in 2019 after he complained about safety problems.

“I don’t know how they have not gotten caught,” he added.

Garda did not agree to interview requests for this story. In a statement to the Times last month, the company said it handles about $8 billion a day for 8,000 clients at more than 75 vaults. It said it has “industry-leading controls in place to monitor the constant movement of our clients’ money.” The company added that the banks’ assets are never at risk because the money is insured.

“Any discrepancies detected are immediately investigated, reported and resolved,” the statement continued. “Inventory reconciliation is normal course of business for any cash vault operation.”

When the Times sent the company a detailed summary of its reporting, Garda did not respond.

Garda’s U.S. operation doesn’t publish a client list. But the Times determined it has held money for at least five of the nation’s 10 largest banks: JPMorgan Chase, Bank of America, Wells Fargo, PNC Bank and TD Bank.

It is not clear which of those banks currently use Garda’s vaults, whether any knew about issues in Garda’s vaults or whether any money is missing today. The banks declined to comment.

The company also stores money for the Federal Reserve, and the Federal Reserve Bank of St. Louis was among the banks that received inaccurate reports because money was missing, according to Bolton, who managed Garda’s St. Louis branch.

The Federal Reserve’s Board of Governors declined to comment, and the St. Louis bank did not respond to interview requests.

We can’t do work like this without you

Dozens of interviews.

A year of reporting.

Help us keep bringing stories like this to you.

Learn more about donatingAs Garda has become a global private-security powerhouse, the company has taken on important and wide-ranging roles far beyond the U.S. currency system. Other divisions of the company provide college campus security and carry out sensitive defense contracts, including protecting the U.S. Embassy in Kabul, Afghanistan.

The Canada-based parent company posts consistently strong operating margins that have allowed it to attract investors and grow at a breakneck pace. In just 15 years, its annual revenue increased from less than $200 million to $2.7 billion. In September, it began its boldest move yet — an ongoing hostile bid to buy G4S, the world’s largest private security firm.

The company’s American armored truck empire is run out of Boca Raton. Its trucks have shuttled money between businesses and Garda vaults across the state, including in Tampa, Miami, Orlando and Jacksonville.

There are indications, however, that the U.S. operation’s growth came at the expense of basic safeguards that are commonplace at other major companies.

A Times investigation published in March described the armored truck business taking shortcuts on maintenance and training. Trucks regularly lacked reliable brakes, seatbelts or even seats. The Times found that hundreds of people had been injured in Garda crashes and at least 19 had died, many in wrecks caused by mechanical failures or driver error. There have been at least three additional fatal crashes since then.

Two former Garda employees say the company attempted to conceal the fallout of its safety problems, as well. The employees — whose accounts have not been previously reported — said they were told to manipulate financial records to downplay the potential costs of those wrecks, increasing the company’s value.

Joseph James, a vice president of finance at Garda’s U.S. arm from 2013 to 2015, confirmed those employees’ accounts and the issues in the company’s vaults.

He said many of Garda’s practices made him uncomfortable.

Extreme cost-cutting helped the company grow quickly, but it also caused problems, he said. And when it came to Garda’s approach to handling money, he said, the problems were big enough to undermine the premise of the business.

“What do you expect an armored car company to be good at?” he said. “Taking care of money.”

‘The bank would not know’

Most major cities have a Garda vault. The biggest ones contain well over $100 million. They operate out of nondescript buildings tucked in industrial city pockets and office parks. The only clue about what happens inside is the armored trucks that roll out of the garage.

Vaults are essentially warehouses piled with money.

Bags filled with bills are kept within secure rooms.

They are usually stored inside moveable metal cages.

A single bag can contain tens of thousands of dollars.

Coins are boxed by denomination and stacked on metal pallets. Each box of quarters contains $500.

Coins aren’t always stored in the vault itself. Instead, they’re often kept behind chain-link fences elsewhere in the building.

Armored trucks pull into the warehouse to load and unload money.

Some of the currency is destined for grocery stores, gas stations and malls. But the armored truck industry has long offered its vaults to banks as well.

In December 2013, Garda scored a deal that helped it jump to the top of that field.

Bank of America, the nation’s second-largest bank, signed a 12-year agreement outsourcing many of its vaults to Garda. The bank sold Garda a large chunk of its existing vault operation, which included 32 buildings and 1,000 employees.

Both parties called it a win. Bank of America reduced overhead costs, and Garda instantly doubled its vault business.

But as Garda boasted about the deal in public, executives in charge of the expansion were discovering a problem: Millions of dollars had gone missing from Garda’s existing vaults, and the company had no idea where the money had gone.

Shellie Crandall, who had been hired to oversee Garda’s vaults several months before the Bank of America deal was announced, was “apoplectic” when she learned multiple locations were missing money, according to James, the finance vice president.

Crandall previously was a vice president at Chase and also spent more than 18 years at Brink’s, where she and James worked together.

James said he watched Crandall relay the news to one of Garda’s highest-ranking officials: Patrick Prince, the chief financial officer for Garda’s operations across the world and second-in-command to Garda’s founder and CEO, Stephan Crétier.

Prince gave Crandall approval to investigate, James said.

Crandall, who left Garda in 2016, declined to comment. Garda did not make Prince available for an interview.

![]() Executive Summary — Out of Balance Condition

Executive Summary — Out of Balance Condition

Executive Summary: This document is to provide data about current known Out of Balance conditions in the CVS vaults and request direction on resolution of all OOB’s to ensure we drive a culture of accountability for losses. In summary, $9,140,279 OOB conditions have been identified and many OOB’s date back to previous years.

The largest potential losses are at the following sites:

LIC ($2.2) MM Lea Blvd ($1.3) MM Needham ($1.2) MM Baltimore ($1.0) MM

Background: The creation and additional CVS infrastructure at the end of 2013 allowed for a focus many operational areas and issues. One focus area was around controls and the mandate to balance each vault and every customer inventory nightly. As the middle management structure was hired/added and their respective CVS sites were visited, it was discovered that the field organization has had known out of balance conditions in several vaults for an extended period of time. Additionally, it was identified that strict adherence to dual control and documented control procedures were not being followed.

In January 2014, , , and Shellie Crandall formed a team to identify, review, report known OOB conditions and provide a framework for clearing or closing (paying) all known OOB conditions. The team members included , , , and various other GW employees. The objective was to identify any known but unreported (to customers) OOB conditions (defined as vault currency/coin did not equal the amount being reported to the customer)

Once the team was formed and tasks assigned, we met weekly to ensure all vault and customer balances were reviewed, out of balances identified, OOB delineated by vault and customer, and the information captured on a central database. Last week the team met face to face and cumulated all information and data and reported OOB conditions in the amount of $9,140,279.

Resolving or paying identified claims is a key priority to ensure site level accountability is reestablished and maintained, customer trust is not eroded, and any financial impacts are realized or accrued for in fiscal year 2014.

Proposed Next Steps:

Research and Reconcile — It is critical we identify resources that can review documentation at the OOB sites and attempt to identify the time and entry error (or theft) that caused the OOB condition. The review will be done to exhaust all efforts in recovering or identifying potential “paperwork” errors versus true loss of funds. The steps listed below is a framework to accomplish this task.

-

Engage Regional Directors’ and require region resources be dedicated to research and resolve all identified OOB conditions. The team’s analysis suggests 3 to 4 resources will need to be dedicated to this project for two months.

- The deliverables of each team would be four-fold.

But the Times obtained an executive summary that outlined what the internal investigation found.

The review aimed to identify every instance where Garda lost money and didn’t tell a customer. The team met weekly. After nine months, it estimated roughly $9 million was missing across Garda’s vaults, according to the document. Some losses had existed for more than two years.

The team flagged four vaults that were of chief concern. The main New York City branch, in Long Island City, was missing $2.2 million. Wilmington, Del., was missing $1.3 million. Needham, Mass., was missing $1.2 million. Baltimore was missing $1 million.

The document urged action. Garda needed to figure out how the money had vanished ...

![]() Executive Summary — Out of Balance Condition

Executive Summary — Out of Balance Condition

-

-

- Assess the identified OOB condition and determine if recovery of the loss amount is feasible.

- Quantify the steps necessary to actually recover the loss or, at a minimum, to remove any financial liability from GardaWorld.

- Implement the Steps necessary to recover the loss, coupled with identification and implementation of Operational Procedures necessary to avoid the situations recurrence in the future.

- Coordinate and/or provide the procedural training and documentation to ensure the site remains in balance moving forward

-

- Assign a project lead to coordinate activities, gather documents and evidence of OOB condition research to present to the Operating Committee for payment review (if applicable). Resource has been identified.

- Assign audit and risk management resource to large OOB conditions to ensure all research and recovery avenues have been explored and employees responsible be identified and held accountable. Audit resources will be required when reviewing the OOB conditions that have existed for more than 2 years and/or are complex to resolve.

Customer Engagement — Once all research has been exhausted, consideration should be given to contact customers and assist their help in resolving any outstanding OOB conditions. This suggestion will need to be explored on a case by case basis and involve the entire Operating Committee for review and approval.

Claims Payment — If an OOB condition cannot be resolved we will need to determine the method of replenishing the customer’s inventory. It is recommended that a finance resource be assigned to own the end to end payment process.

Closing: Please review the information and provide suggestions and input on the suggested approach to resolving the identified OOB conditions.

... hold accountable whoever was responsible, consider telling some customers and replace the money.

But interviews with former Garda employees and other records show that Garda continued having shortages.

From:

Sent: Thursday, January 22, 2015 3:06 PM

To:

Cc:

Subject: RE: TD Bank - Stratford Coin

Good Afternoon,

The Stratford terminal stopped handing our CVS work some time ago, but our coin inventory remains. Since there has been no activity for quite some time, I would like to have the remaining coin inventory transferred to LIC as soon as possible. Our currency was removed just after the work was transferred to LIC.

Can you have this arranged for us or put me in contact with someone who can?

Thanks and have a great day!

Currency Management Analyst, Officer

TD Bank, America’s Most Convenient Bank

NJ5-002-108 | 6000 Atrium Way, Mt. Laurel, NJ 08054

T: | F:

In February 2015, the coin operations manager for Garda’s bustling New York branch exchanged emails with the company’s internal audit department about TD Bank’s request to move its coin inventory from Connecticut to New York, according to the emails, which were reviewed by the Times.

From:

Sent: Friday, January 23, 2015 10:47 AM

To:

Cc:

Subject: RE: TD Bank - Stratford Coin

Our LIC Coin Manger has contacted to begin the process. Once has the TD Inventory from Stratford and it has been verified, we will begin the transition.

and/or I will keep you posted on the progress.

Thanks

Associate Director, Northeast CVS, Cash Services

The coin operations manager told TD Bank that Garda would begin the process. But inside Garda, there was concern.

From:

Sent: Monday, February 02, 2015 11:22 AM

To: GardaWorldAudit

Cc:

Subject: RE: TD Bank - Stratford Coin - Shortage $924 000 - IMPORTANT

Good Morning,

See attached email from TD that was sent out today, we have to get back to the bank.

Thanks,

Coin Operations Manager

5-26 45th Ave

Long Island City NY 11101.

Office Ext

The subject line of one of the emails laid out the situation: “TD Bank — Stratford Coin — Shortage $924,000 — IMPORTANT.”

From:

Sent: Friday, January 30, 2015 5:12 PM

To: GardaWorldAudit

Cc:

Subject: RE: TD Bank - Stratford Coin

Good afternoon,

Can someone please advise TD bank is asking to transfer and close out their coin inventory from Stratford to LIC, but there is a big discrepancy and we need to get the bank an answer on when we can move the inventory to LIC.

It’s a difference off $924,450.60

Bank : 0004 Site : STRA Date : 01/29/2015

| Beginning | Incoming | Outgoing | Ending Total | ||

|---|---|---|---|---|---|

| 10 FIT | Half | 31546.00 | 0.00 | 0.00 | 31546.00 |

| 11 FIT | Qtr | 942022.00 | 0.00 | 0.00 | 942022.00 |

| 12 FIT | Dime | 130115.60 | 0.00 | 0.00 | 130115.60 |

| 13 FIT | Nickel | 17824.05 | 0.00 | 0.00 | 17824.05 |

| 14 FIT | Penny | 133764.95 | 0.00 | 0.00 | 133764.95 |

| 15 FIT | Sba | 106503.00 | 0.00 | 0.00 | 106503.00 |

| 22 FIT | XCoin | 10.00 | 0.00 | 0.00 | 10.00 |

| COIN | Total | 1,361,775.60 | 0.00 | 0.00 | 1,361,775.60 |

This is the coin total that’s in Stratford for TD...

TD coin total

| 18 SBA | $18,000 |

| 86 Halves | $ 43,000 |

| 607 quarters | $303,500 |

| 74 dimes | $18,500 |

| 12 nickels | $1,200 |

| 2125 pennies | $53,125 |

| Total | $437,325 |

Coin Operations Manager

5-26 45th Ave

Long Island City NY 11101.

Office Ext

Roughly $924,000 of the bank’s coins could not be found.

From:

Sent: Monday, February 02, 2015 3:32 PM

To: GardaWorldAudit

Cc:

Subject: RE: TD Bank - Stratford Coin - Shortage $924 000 - IMPORTANT

Team,

See 2nd email sent by the bank today.

Can we move the coins over to LIC from Stratford and report that the coin has been transfer to LIC and work on the shortage internally; in this way the bank would not know that there is a discrepancy?

Coin Operations Manager

5-26 45th Ave

Long Island City NY 11101.

Office Ext

In one of the emails, the manager suggested that Garda could tell the bank the money had been moved and “work on the shortage internally.”

“In this way,” she wrote, “the bank would not know that there is a discrepancy.”

From:

Sent: Monday, February 02, 2015 3:45 PM

To: GardaWorldAudit

Cc:

Subject: RE: TD Bank - Stratford Coin - Shortage $924 000 - IMPORTANT

By doing the transfer, the shortage will technically be transferred from Stratford to LIC so please keep a paper trail or trace of that transaction somewhere.

Yes this will be documented properly, I will report what is physically sent to me from Stratford, but recon will report what they have been reporting to TD, in this way the shortage will show in my physical coins.

Otherwise, how are you going to transfer the whole amount requested by TD?

It's impossible to transfer the whole amount when there is a huge shortage, I'm just trying to avoid the bank from being suspicious or unless someone will notify the bank that there is an issue.

This is just my opinion I could be wrong but the bank is requesting an answer today.

Thanks,

Coin Operations Manager

5-26 45th Ave

Long Island City NY 11101.

Office Ext

In another, she continued: “It’s impossible to transfer the whole amount when there is a huge shortage, I’m just trying to avoid the bank from being suspicious or unless someone will notify the bank that there is an issue.”

It is unclear what actions the company took. The audit department told her to “get the proper approval and directive since this involves a significant shortage.”

James, the former vice president of finance, said the scale of the problem across the company meant the issue couldn’t be written off as a few bad employees.

James witnessed internal audits that found vaults were short. Vault managers told him they had shown auditors money that belonged to other banks. He didn’t see another explanation for how Garda continued to pass the banks’ routine audits. It was clear that banks were being kept in the dark, James said.

“I can remember some of these vault managers being near nervous breakdowns over the state of where their vault was,” he said.

Missing money

Former Garda employees — from armored truck drivers to higher-ranking managers — described feeling shocked by how little Garda did to keep track of the money in its care.

Former managers told the Times that employees had ample opportunity to steal. The footage from some Garda security cameras was of such poor quality that it looked like it had been shot through frosted glass. Some cameras had no ability to zoom.

Thefts sometimes went unnoticed until a client pointed out that money was missing, making the crime harder to solve.

In 2012, Garda lost $76,000 during a delivery in Springfield, Mass. The company didn’t investigate until a month later, then accused two employees of stealing the money.

Garda told police it had the theft on video. But the company couldn’t provide the video or other evidence, court records show. A judge dismissed the criminal charges against the employees.

Theft was rampant in that branch, according to emails between Garda managers and company security. Vault employees accused one co-worker of stealing money by stuffing it in her bra and shoes. Another Springfield employee stole $30,000 over a three-month period. A third told Garda investigators he was left alone with open bags of money. He said he couldn’t resist the temptation and had snatched at least $71,900 over several months.

Erik Quinn, who worked in the Springfield vault in 2014 and 2015, recalled constant problems, especially with coins.

He and other employees said that coins were handled less carefully than bills. Some blamed the fact that coins are heavy and cumbersome.

Quinn said some banks would have too much money and some would come up short. Garda moved money from customer to customer and hoped it would add up later, he said.

“It was shifting money around and it was almost controlled chaos,” he said. “But they couldn’t control the chaos.”

In 2013, in Montana, three bags of money — containing $390,000 — disappeared off a Garda truck. Garda couldn’t figure out how the money went missing. But an ex-employee started spending lavishly in Las Vegas and turned up at a bank with a shoebox full of cash.

In 2020, the employee was convicted of money laundering and the transportation of stolen money in connection with the crime.

But federal prosecutors didn’t charge the employee with actually stealing the cash. At trial, they admitted they didn’t know when or where the money was taken, or who took it.

Camera coverage that could have documented the theft didn’t exist. A former Garda employee testified that truck doors could be popped open with a broom handle. Trucks were left unattended, the prosecutor noted, even though that’s against Garda’s policy.

“This is a strange case in some ways, because there’s some unknowns,” the prosecutor said in his closing statement. “A lot of unknowns, actually.”

A detective testified that employees regularly didn’t follow Garda’s money-handling policies. The detective said she knew this because her caseload included five other unsolved Garda thefts.

Brian Fink, who worked on a “SWAT team” that the company sent to branches having operational problems, also said the company was plagued by thefts it couldn’t solve.

Fink, who worked for Garda from 2016 to 2017, later became a branch manager. He said he left Garda under pressure after he tried to fire two employees, who then accused him of pulling his weapon on them in a room that lacked cameras.

Every branch Fink visited as a member of the SWAT team — including West Palm Beach, Philadelphia, Atlanta, St. Louis and Columbus, Ohio — did the job a little differently. But across the company, he saw similar problems: broken-down or subpar equipment and poor protocols that made it easy to lose track of the cash.

The company’s rules said that workers could not leave for the night until every bill and coin was accounted for. But Fink said he hardly ever saw that happen at Garda.

“I don’t know why anybody would have them take their money,” Fink said.

James said that when he was at Brink’s, no one went home until the vault was balanced. At Garda, he said, that often wasn’t the case.

James said he was shocked by how much Garda spent paying claims related to thefts, given the size of the business. It was unlike what he’d seen at Brink’s, he said.

Bolton described the St. Louis vault as in constant disorder.

“At the end of the night, I would be freaking out about thousands (of dollars) missing, and other people weren’t,” Bolton said. “When there was a shortage or an overage it wasn’t a big deal because it happened just that often.”

Bolton said on multiple occasions he was asked to send money to another branch to cover shortages. At least once, he said, money was sent to his branch.

He found the practice dishonest and said it bothered him.

Tricking the auditors didn’t always work, he added, and some banks complained about repeated issues.

Both bank and retail clients sometimes gave Garda extra money by accident, he said. The currency would be moved into what Garda employees called the “99 account.”

Three other former employees in different cities described similar accounts that Garda used to store money of unknown origin.

“It’s just money sitting there, where nobody knows where it goes and nobody can explain why it’s there,” Fink said. “Technically, in a cash industry, there should be no leftover money.”

Fink and Bolton both said Garda sometimes used it to cover shortages.

The role of the banks

The U.S. government requires that banks keep meticulous track of customers’ money, even if they outsource its handling to another company.

“It’s still the bank’s vault, from our perspective,” said Kevin Greenfield, deputy comptroller for operational risk policy at the Office of the Comptroller of the Currency, which regulates national banks. “They need to make sure it is operated in a safe and sound manner.”

Greenfield was speaking generally, not about Garda. Through a spokeswoman, he later declined to comment on the Times’ specific findings.

The Federal Deposit Insurance Commission requires banks to have enough security in place to identify thieves and “preserve evidence that may aid in their identification and prosecution.”

Recurring vault imbalances are seen as “very risky” by banks, said Pete Soraparu, a retired banking executive and former executive director of banking think tank BAI.

“Not having a teller drawer balance is a bad thing for a bank, so if your cash vault isn’t balancing, that’s a huge issue,” he said.

Told about the Times’ reporting on Garda’s vaults, Soraparu said “that’s crazy” and described the situation as “very troubling.”

Public examples of bank vault contractors hiding losses are rare. The Times was able to identify only one case, from the 1990s, when federal prosecutors accused Revere Armored of not telling the banks that used its vaults that millions of dollars had gone missing.

According to court records, Revere sent banks fraudulent balance sheets and physically moved money from account to account to fool auditors.

The fraud wasn’t discovered until a competitor filmed Revere drivers leaving trucks unattended and told the company’s insurer. The insurer dropped the company, and the insurer’s investigator tipped off the FBI, leading to the vault problems coming to light.

The couple that owned Revere claimed to be victims of rampant internal theft. Prosecutors said the couple had taken the cash to fund their personal gambling habit.

The case made national headlines, and the couple went to prison for bank fraud. But the attorney assigned by a judge to split up the money concluded the banks shared some fault for the disappearance, according to a report in the New York Times. The banks should have done more to hold Revere accountable, which would have been easy through joint audits, he noted.

Revere lost an estimated $35 million. In the end, the attorney recommended the banks eat the losses.

Inaccurate financial reports

Garda has also faced allegations that it uses deceptive financial practices in other areas of its business.

In 2008, former Garda executive Richard Irvin alleged in a wrongful termination lawsuit that the company had concealed serious financial troubles by publicly reporting inaccurate numbers related to its U.S. armored truck business.

The lawsuit said that Crétier, Garda’s founder and chief executive officer, told a meeting full of executives that he ran one of the world’s largest investigative operations and if anyone leaked how bad the company’s finances were, he’d find out. According to the lawsuit, he added: “I will kill you, and I will kill your family.”

In a deposition, Crétier admitted he threatened to kill any executives who leaked information. But he testified that he was joking and denied threatening to kill family members.

In a motion, Garda’s attorneys described Irvin’s financial allegations as an “absurd theory.” The case settled before trial.

In 2016, Christine Bouquin, who oversaw risk management for Garda, sent an email to her supervisor detailing widespread safety problems at the company, as the Times reported in March. But in that email, which was filed in public court records, Bouquin also accused the company of “material misrepresentation of our financial condition.”

Garda sets money aside to pay legal claims related to crashes and workers compensation, based on estimates of what each case might eventually cost. Manipulating these numbers — called “reserves” — can alter a company’s financial outlook.

Bouquin, who worked at Garda from 2012 to 2016, wrote in the email that she was directed to lower those estimates around financial reporting deadlines.

This could improve Garda’s financial picture by “millions, if not tens of millions, of dollars,” Bouquin wrote.

Other instructions coincided with major financial transactions. For example, Bouquin said, she was told to increase the amount in reserves — making the company look worse — just before Crétier bought back the company’s stock to take Garda private.

“The continuous manipulation of financial records, seemingly to drive a bottom line goal, is unlike anything I have experienced in my 20-plus years of professional experience,” she wrote.

Garda laid off Bouquin the day after she sent the email. Earlier this year, Garda’s attorneys called her untruthful and said she has a “personal bias against GardaWorld.” The company has sued Bouquin to get her to return company documents. Bouquin has become an outspoken critic of the company, writing posts on LinkedIn about Garda’s safety practices and accusing the company of trying to intimidate her into silence.

Bouquin told the Times she was given specific numbers to hit. She provided emails where she and others in her department raised concerns about these practices before she was terminated.

In a September 2016 email, LaJessica Mathis, who worked as a risk management specialist, wrote to Bouquin and a finance employee: “As you may be aware, our previous executive directive required that we keep our reserves as low as possible, for as long as possible.”

She added: “A notable portion of the reserves are not very reliable in regards to accurate forecasting.” She pointed to cases where the reserves seemed inaccurate and asked if the current executive leadership wants to use these numbers or “accurate financials.” The emails do not show whether Mathis got an answer. Mathis said she was laid off from Garda later that month. Eventually, Garda eliminated the risk department.

Mathis told the Times that the company constantly expected the risk department to reduce reserves, to a degree that she felt they were a “bold lie.” She said the department kept two sets of books, one with numbers she felt were realistic and another that followed the marching orders to estimate lower costs.

In another email, a member of the risk department listed specific examples of Garda crashes that he said were more serious than the amount the company had set aside would indicate.

One was a 2013 Los Angeles crash where a 38-year-old Garda driver’s seatbelt failed. The aspiring nurse was thrown into the windshield, causing permanent brain damage.

According to the email, the company had valued the case at $234,000. The risk department believed it actually would cost $2 million to $3 million — if not more.

A second case was valued at $33,000 but was likely to cost more than $200,000, the email said.

A third was listed at $45,000 but involved an accident that had led to medical bills exceeding $340,000. The real cost was expected to exceed 10 times the official estimate.

James, the former vice president of finance, confirmed Bouquin’s account. He was once Bouquin’s supervisor and said Garda’s insurance reserve strategy and high number of claims were regularly discussed by senior management.

He said Garda hired “very good” consultants to help handle claims.

“Their opinion was shared with Christine,” James said. “And there was constant pressure on her, direction to her even, to keep below those estimates — because that’s a hit to earnings.”

There were signs that Wells Fargo, one of Garda’s contractors, found the strategy unusual.

In 2014, Bouquin sent an email to a senior claims consultant at Wells Fargo in Tampa, asking for guidance. At the time, the company was helping Garda manage its insurance policies.

Bouquin asked for help describing the company’s method of valuing claims.

Bouquin told the Times she was trying to get Wells Fargo to take action. “I wasn’t going to falsify records and was pretty much at the end of my rope as to what could be done internally,” she said. “We were working with Wells Fargo, so I kind of punted a hot potato over to them.”

Wells Fargo declined to comment on its work for Garda, aside from saying it had sold that part of its company and that the employee Bouquin emailed no longer worked for the bank.

But in response to Bouquin, the Wells Fargo claims consultant wrote that she had been “wracking my brains over this one” and discussed it with a co-worker.

She told Bouquin that she and her co-worker ultimately decided to remove references to Garda’s method of calculating reserves from the company’s documents. She continued: “That way, we don’t put in writing anything that could potentially cause Garda embarrassment or trouble explaining.”

‘Winning’

Garda touts itself as a runaway success. It posts strong profit margins and has attracted investors while steadily buying competitors.

The company already operated armored trucks in Canada when it entered the U.S. market in 2005. Crétier, the chief executive, thought the big U.S. players, Brink’s and Loomis, were weak and mismanaged, he said in a deposition. He saw a special opportunity in the fact that American banks mostly hadn’t outsourced their vaults, whereas nearly all had in Canada.

At the time, Garda was expanding rapidly. The international company’s annual revenues grew from $200 million in January 2006 to $880 million in January 2008.

Much of the growth came from acquisitions, financed with huge amounts of debt. Concerns about Garda’s ability to pay began to drag down the company’s stock prices. Some analysts predicted Garda’s demise.

In 2012, Crétier took the company private with the help of private equity firm Apax Partners. Apax sold its stake to private equity firm Rhône Capital in 2017, and Rhône sold to BC Partners in 2019. Today, 51 percent of the company belongs to BC Partners, with Crétier and other top executives owning the rest.

Garda has continued to expand, completing at least 10 major acquisitions in 2018 and 2019 alone.

By January 2020, the international company’s annual revenues were roughly $2.7 billion, and the U.S. armored truck division’s revenues were about $585 million. The company says its operating profit has grown for six years straight.

It has bought two additional security companies since March and is embroiled in an intense public-relations campaign relating to its hostile takeover of G4S, with Garda executives alleging the much bigger company is mismanaged and G4S calling Garda’s offer “highly opportunistic.”

But even as Garda pursued deal after deal, the company’s executives didn’t want to pay for the basics needed to run the business it already operated, former managers said.

As a vice president of finance, James oversaw accounts payable. He said Garda’s U.S. operation constantly didn’t have enough money to pay its bills, in part because profits were needed to satisfy large debt payments.

He said issues with truck safety and vault security had the same cause: Fixing either would require money. The priority, he said, was making money, not spending it.

“What this really goes to is the state of the investment in the infrastructure of the company,” James said. “If we are going to be a low-cost provider, what cost are we going to cut out of the business?”

Crétier has acknowledged his business model sometimes leaves the company strapped for cash.

“It's a working-capital business,” he said in a January interview with the podcast Speaking of Business. “The more you grow, the more you're almost bankrupt.”

The company has faced bankruptcy four times, Crétier said, adding that the fear of bankruptcy loomed “even when business was going extremely well, and I was really growing.”

Nonetheless, Crétier has continued to describe Garda as a resounding success. “Winning is in GardaWorld’s DNA — we’ve put it to work by transforming the security market,” he said over the summer.

And the company has rewarded Crétier handsomely. In June, Garda reported paying him a $2 million bonus in acknowledgement of how well he ran the company.

Times data reporter Connie Humburg contributed to this report.

We can’t do work like this without you

Times reporter Bethany Barnes has been investigating GardaWorld for more than a year, with important contributions from data reporters, editors, copy editors, designers, visual journalists and digital producers.

Investigative journalism like this is the most expensive work that we do.

Please consider supporting us with a tax-deductible donation to the Tampa Bay Times Investigative Fund.

Learn more about donatingOr, become a long-term supporter:

Subscribe to the TimesAbout the reporter

Bethany Barnes

Bethany Barnes has been an investigative reporter for the Tampa Bay Times since 2019. She previously worked for the Oregonian, the Las Vegas Review-Journal and the Las Vegas Sun.

Send a confidential tip: Have you had experiences with Garda you’d like to share? Send a confidential message to Times investigative reporter Bethany Barnes via email at [email protected] or encrypted email at [email protected]. Signal message 727-892-2944 or text or call 503-714-6476. Send mail to Bethany Barnes, 490 First Avenue South, 3rd Floor Newsroom, St. Petersburg, FL 33701.

If you have a different topic to discuss with one of our investigative reporters, visit https://www.tampabay.com/tips.

Additional credits

- Editor: Adam Playford

- Print design Sean Kristoff-Jones

- Digital design Martin Frobisher

- Copy editing Peter Couture